Three Numbers Every Woman Should Know

Women today are navigating money, work, family, and longevity in ways that look very different from previous generations. You’re building wealth, leading households, caring for others, and very often, carrying the long-term financial responsibilities for your family. At KDI Wealth, we walk alongside many women who are juggling these roles every day. And while every woman’s story is unique, we’re seeing three numbers shape the financial reality for most of them: 5. 45. 59.

These numbers tell a powerful story about longevity, wealth, responsibility… and why thoughtful planning matters now more than ever.

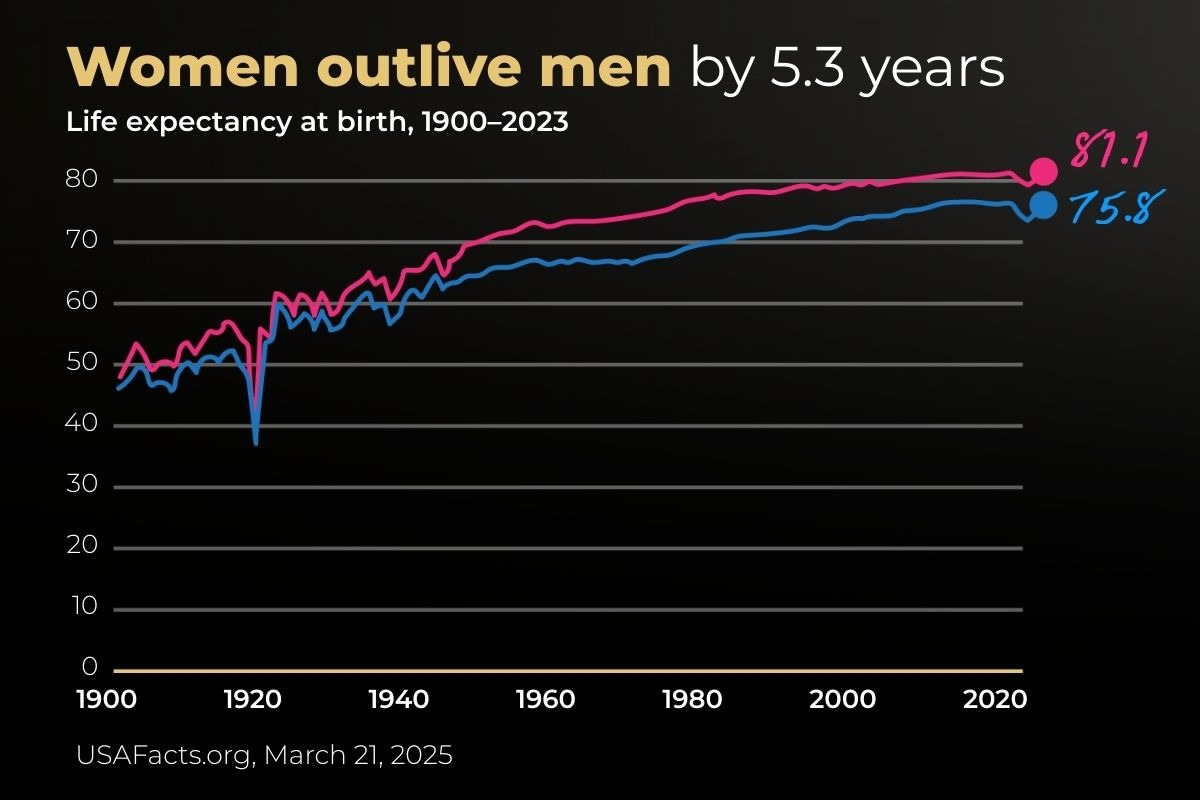

5: The Extra Years Your Money May Need to Last

On average, women in the U.S. live five years longer than men. In 2023, life expectancy was about 75.8 for men and 81.1 for women.¹ Longer life is a gift—but it also means your wealth must support you for more years, often during a time of increased healthcare needs.² This has real financial implications: - Retirement may last 30 years or more - Healthcare and caregiving costs often rise in later decades - Career pauses for caregiving can reduce lifetime earnings and savings

How can women financially prepare for a longer life? At KDI Wealth, we often encourage women to consider:

- Plan as if you’ll live to at least 95. It’s much easier to adjust when resources last longer than expected than the other way around.

- Use a “time‑bucket” strategy. Set aside assets for short-term needs, long-term growth, and dedicated healthcare or extended‑care costs.

- Stress-test your plan. Ask: What happens if I live longer? If healthcare costs spike? If markets underperform? These conversations build confidence—and flexibility.

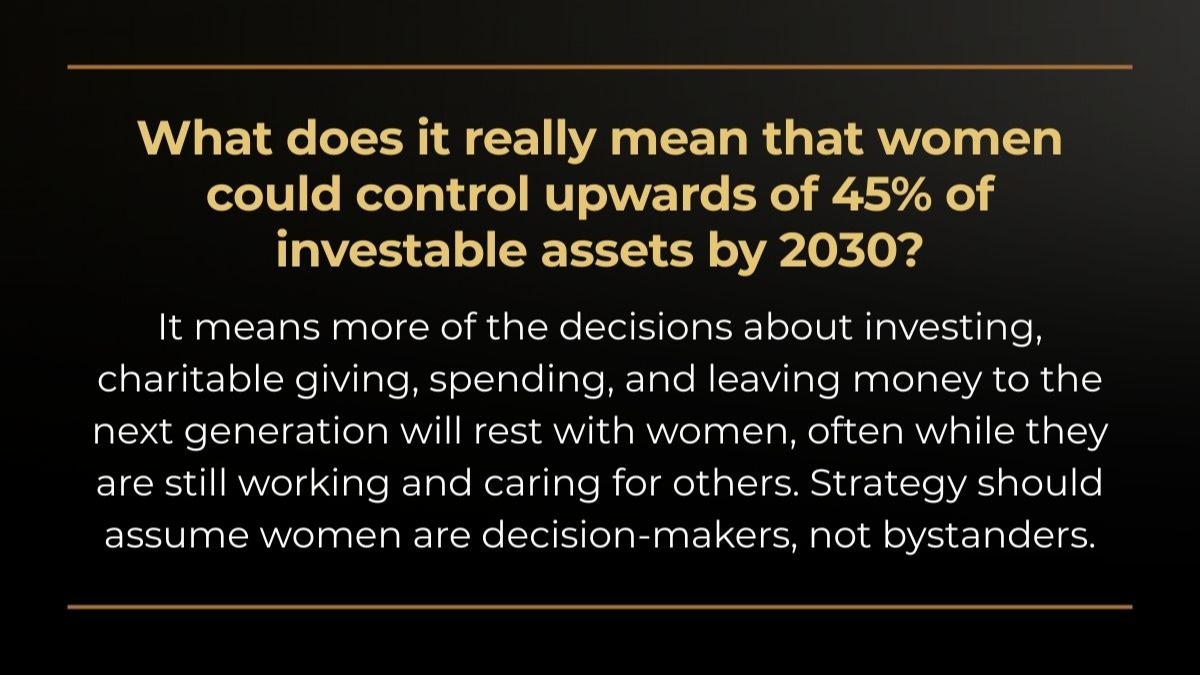

45: The Percentage of Investable Assets Women May Control by 2030

Women are on track to oversee 45% of all investable assets in the U.S. and Europe by 2030.³ A major reason? The multi‑trillion‑dollar wealth transfer from Baby Boomers. Estimates suggest that 70–80% of this generational shift will go to women.⁴ At the same time, women’s income power continues to climb: - 16% of opposite-sex marriages now have wives as the primary or sole breadwinner, triple the share from 50 years ago⁵ - In 29% of marriages, both spouses earn about the same⁵ - In 2023, 45% of mothers were breadwinners, with another 24% as co‑breadwinners⁶ Women aren’t just inheriting money, they’re earning it, growing it, and directing it.

What does this mean for your financial strategy?

Whether you’re single, married, a caregiver, or preparing to inherit, it may be time to ask:

- Does your portfolio reflect your goals and comfort with risk?

- Does your financial plan center around both partners’ income—or only one?

- Are estate documents updated so the surviving spouse has decision-making clarity?

Three helpful steps to consider:

- Create or update an Investment Policy Statement. Think of it as the roadmap for your wealth—clear, intentional, and customized.

- Consolidate scattered accounts. It’s much easier to plan when everything is visible and coordinated.

- Right-size your safety net. If you’re the primary earner, your insurance and savings strategy should reflect that reality.

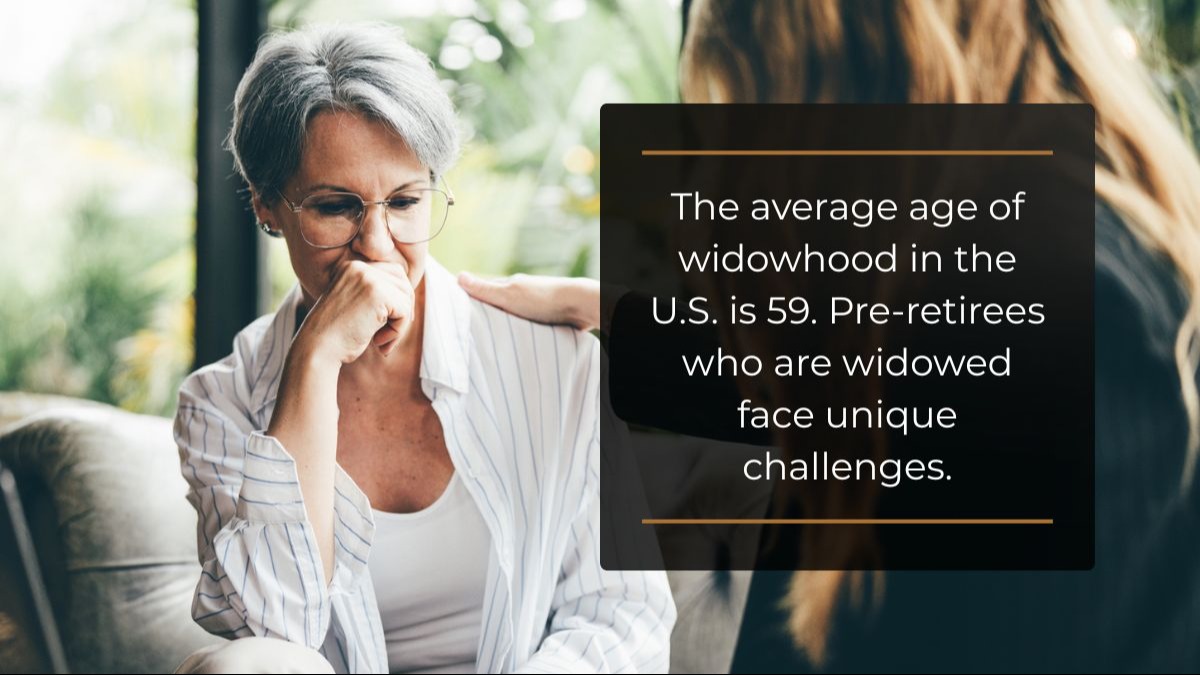

59: The Average Age Women Become Widows

It’s a difficult topic, but also an essential one: The average age of widowhood in the U.S. is just 59.⁷ ⁸ And the ripple effects are significant:

- Nearly 700,000 women become widows each year

- Women spend an average of 12–13 years as widows

- Household income often drops 37–50% after a spouse’s death

- 40% of widows don’t feel confident managing finances alone

- Women who worked with a financial professional before widowhood are 90% more likely to feel prepared

This isn’t about fear, it's about readiness, clarity, and peace of mind.

A helpful way to think about widowhood planning: Clarity. Control. Continuity.

Clarity - Keep an updated list of accounts, documents, passwords, and contacts - Review it together as a couple

Control - Consider joint ownership where appropriate - Make sure both spouses understand retirement income, taxes, and cash flow

Continuity - Build relationships with trusted professionals before a crisis - Involve adult children or trusted family members in the planning process

Bringing It All Together

Many women today are:

- Contributing significantly, or equally to household income,

- Building assets in their own names,

- Likely to outlive their partners,

- Supporting both children and aging parents

- This creates a unique financial landscape, one that deserves a strategy tailored to your real life, not just your numbers.

A few questions to ask yourself:

- If my income stopped due to illness, could my family stay financially stable?

- Do my documents and account titles reflect the role I play today?

- Does my financial strategy honor the emotional, mental, and practical load I carry?

And potential next steps:

- Talk with a financial professional about the plan that supports your life today and tomorrow

- Consider a “career resilience fund”, a slightly larger emergency cushion

- Review account ownership, beneficiary designations, and estate structures

Why Work With a Financial Professional?

These three numbers: 5, 45, and 59 aren’t just statistics. They shape the way women live, care for others, and plan for the future. You don’t have to navigate these questions alone. Many women gain confidence, clarity, and peace of mind by partnering with a professional who understands the full picture. If you’d like to explore what these numbers mean for your own financial story, we’re here ready to listen, and ready to help.

Sources

1. USA Facts, March 21, 2025

https://usafacts.org/articles/do-women-live-longer-than-men-in-the-us/

2. The Guardian, December 11, 2024

https://www.theguardian.com/us-news/2024/dec/11/americans-living-with-diseases-health-study?

3. McKinsey & Company, May 8, 2025

https://www.mckinsey.com/industries/financial-services/our-insights/the-new-face-of-wealth-the-rise-of-the-female-investor

4. Diversified Trust, October 13, 2025

https://diversifiedtrust.com/blog/women-and-wealth-transfer/?

5. Pew Research Center, April 13, 2023

https://www.pewresearch.org/social-trends/2023/04/13/in-a-growing-share-of-u-s-marriages-husbands-and-wives-earn-about-the-same/?

6. Center for American Progress, May 9, 2025

https://www.americanprogress.org/article/breadwinning-women-are-a-lifeline-for-their-families-and-the-economy/

7. Gitnux, December 11, 2025

https://gitnux.org/widowhood-statistics/

8. Resto NYC, October 12, 2023

https://www.restonyc.com/how-long-is-the-average-woman-a-widow/